Gold remains under increased pressure ahead of FOMC decision and more important remarks from Powell

Gold holds in red for the third consecutive day, pressured by growing fears that elevated oil prices would lift inflation and prompt Fed to take more hawkish stance on monetary policy.

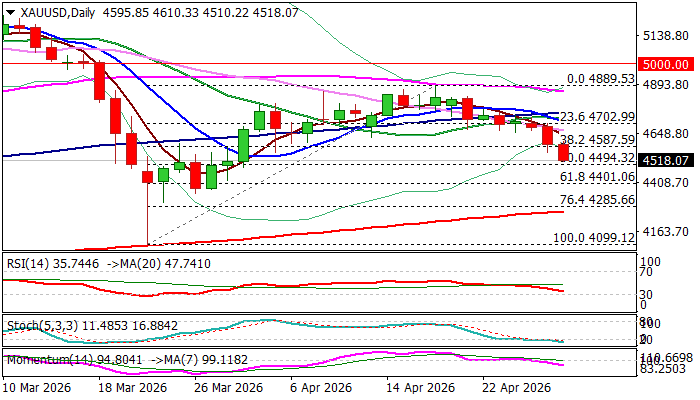

The yellow metal remains in defensive since mid-April ($4889 recovery peak) and has so far retraced over 38.2% of $4099/$4889 recovery leg, with weakening daily studies (10/100; 10/20DMA bear-crosses / strengthening negative momentum) opening prospects for deeper drop.

Bears face immediate targets at $4500/$4494 (psychological / 50% retracement) where headwinds could be expected due to oversold conditions, but upticks are likely to be limited (ideally to be capped under $4600 zone) and keep protected the most significant barrier at $4702 (daily Ichimoku cloud base).

Clear break of $4500 zone to open way towards $4401 (Fibo 61.8%) and unmask 200DMA ($4264).

With situation in the Middle East remaining fragile, traders shift focus towards Fed policy decision (due later today) and more important remarks from Chief Powell (as the central bank is widely expected to stay on hold this time) to estimate the depth of the impact from the war and signals of Fed’s direction in coming months.

Overall picture should remain negative in case of persisting uncertainty or escalation in the Middle East, as this would also accelerate Fed’s action on interest rates and likely shift narrative towards fresh policy tightening.

Res: 4587; 4632; 4702; 4725

Sup: 4494; 4401; 4351; 4264