Dollar remains in red on growing signs of Fed easing pace of hikes; US job report in focus

The dollar index remains at the back foot in early Friday and hit new lowest since early July, in extension of Thursday’s 0.82% drop.

Data released on Thursday showed solid growth in consumer spending, while the number of Americans filling for employment benefits declined, signaling that the labor market, one of the four pillars of the economy, remains resilient.

Although the picture was overshadowed by weaker than expected manufacturing PMI, which showed contraction in the sector for the first time in over two years.

Solid numbers add to cautious optimism that expected recession next year would be milder and shorter, boosting hopes that the peak in interest rates could be near that fuels headwinds to the Fed’s recent aggressive steps in policy tightening.

Markets await release of US November jobs report later today, which is expected to provide more clues about the situation in the labor market and the impact of rate hikes.

US non-farm payrolls forecast increasing by 200K new jobs in November, compared to 261K in October, signaling that job growth in November was likely the smallest in almost two years, though recent data showed 1.7 job openings per unemployed person, adding to signals that US labor sector remains tight.

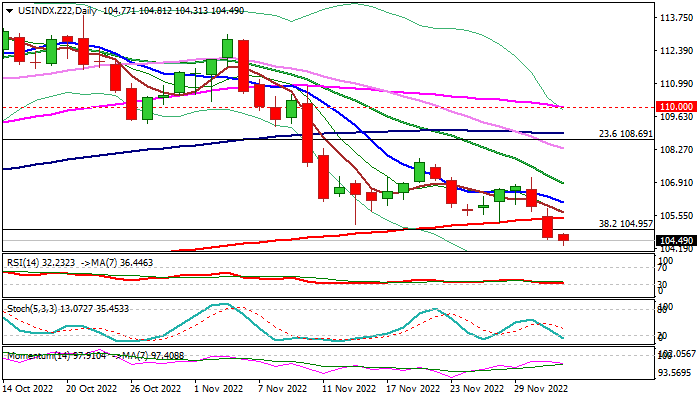

Technical view

Bears remain fully in play on daily chart, as Thursday’s close below pivotal supports at 105.44 (200DMA) and 104.95 (Fibo 38.2% of 89.15/114.72) generated fresh bearish signals, which will be confirmed on a weekly close below these levels.

Also, November’s massive bearish monthly candle continues to weigh heavily on the action, contributing to scenario of deeper correction of larger uptrend from Jan 2021 to Sep 2022.

Near-term action probes through supports at 104.49 (Aug 10 trough / Fibo 76.4% of 101.29/114.72 bull-leg), break of which would unmask targets at 101.30 zone (top of ascending daily Ichimoku cloud / May 30 higher low).

Broken Fibo support at 104.95 and 200DMA (105.44) reverted to resistances, with the latter to ideally keep the upside protected and guard upper pivots at 106.86 (falling 20DMA) and 107.13 (Nov 30 lower top).

Res: 104.95; 105.44; 106.08; 106.86

Sup: 103.83; 103.40; 103.18; 101.94