US inflation and Omicron impact seen as key factors for dollar

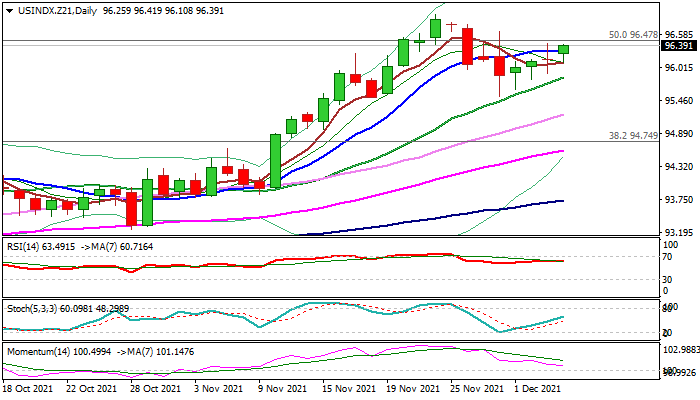

The dollar index regained positive tone after a pullback from new 2021 high (96.92) was contained by Fibo 38.2% retracement level of 93.24/96.92 upleg, that marks a healthy correction of the recent advance, which accelerated on rising hopes of Fed’s faster tapering and earlier than expected first post-pandemic rate hike.

Initial euphoria somewhat faded following softer tone from the US central bank in past two policy meeting, but fresh hawkish twist has been noted from Fed chief Powell’s latest remarks.

Surging inflation increased pressure on Fed to fasten the process of policy normalizing, although the policymakers continued to describe current high price pressures as transitory and refraining to act, despite high market expectations.

The Fed focuses on the labor market which struggles to recover from pandemic sharp drop and the central bank pointed full recovery in labor sector as one of key requirements for a rate hike.

Investors focus on Friday’s US CPI data, with release close to forecast (Nov 4.9% f/c vs Oct 4.6%) to add to supporting factors for Fed’s December policy meeting, due next week.

In this case, the central bank is likely to announce faster tapering that would lead towards earlier start of policy tightening.

However, markets keep an eye on the situation with new Omicron variant of coronavirus, hoping that it is less deadly than current Delta variant that signal the US will refrain from lockdowns and brighten prospects for the Fed.

Fresh recovery leg is tracked by rising 20DMA (95.85) which marks pivotal support that maintains bullish bias for test of 96.92 peak, break of which would open way for extension towards targets at 97.60 and 98.20 (July’s high / Fibo 61.8% of 103.80/89.15 fall).

Res: 96.64; 96.92; 97.45; 97.78

Sup: 96.11; 95.85; 95.22; 94.75